Eurobonds market feels like war is over

Teniz Capital Investment Banking has released a review of Ukraine’s sovereign bonds

According to the analysts, in recent days the market has been undergoing a reassessment amid news about possible negotiations and a peace agreement. In an interview with Roza Aigistova, Deputy Director of the Trading Department at Teniz Capital Investment Banking JSC, we decided to take a closer look at the current situation surrounding Ukraine’s sovereign bonds against the backdrop of investors regaining confidence in a potential de-escalation of the military conflict.

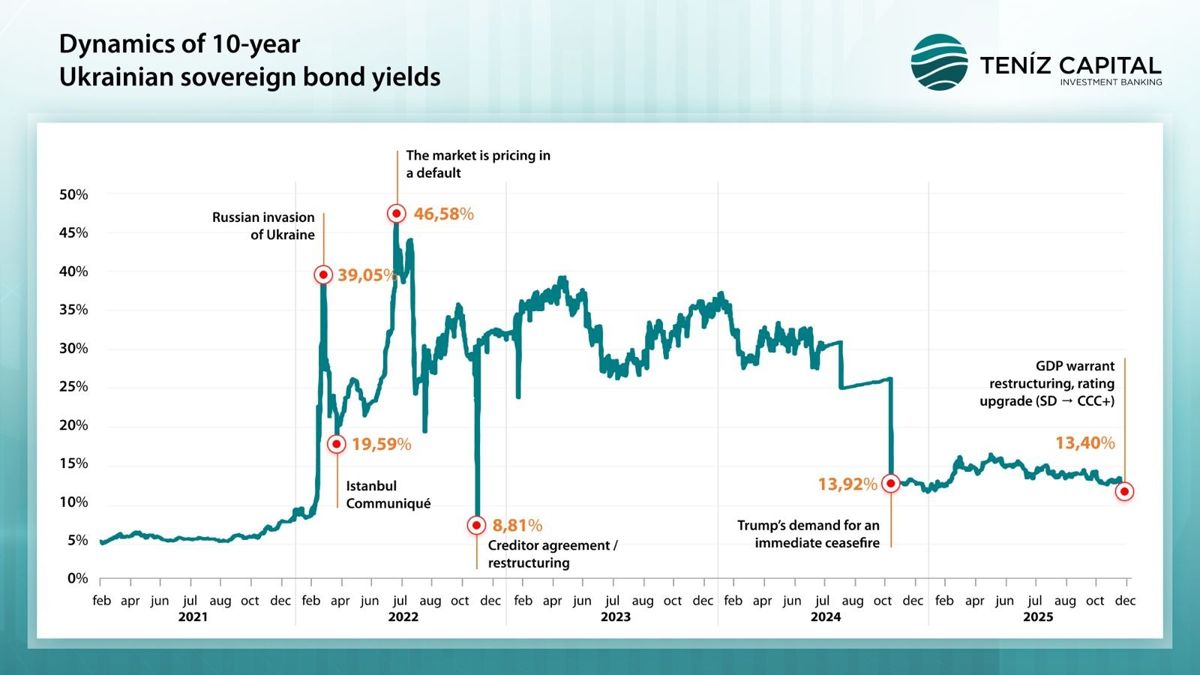

Analysts believe that Ukrainian bonds remain an instrument with an extremely high level of risk. Prices of Ukrainian bonds had been depressed because the war and its associated risks were expected to be long-lasting, requiring investors to price in a high probability of payment difficulties and severe losses. Now the situation is changing. News and discussions about possible negotiations have prompted the market to consider that the economy may gradually recover. Could you elaborate on this?

— Before 2022, Ukraine’s 10-year sovereign bonds were trading at around 100–110% of face value. Following Russia’s invasion of Ukraine at the end of February 2022, prices collapsed, falling to 19–20% in early March, reflecting a scenario of deep credit stress and expectations of default. What followed became even more interesting, as further price movements were driven not by classical economic fundamentals but by trading on expectations: negotiations, restructuring, political signals, and hopes for de-escalation. In other words, from local lows in the range of 15–20% in March–July 2022, bond prices rose more than threefold to a peak above 62% by late 2025 — early 2026, which corresponds to an increase of around +200% purely due to risk repricing.

If we translate this into numbers, what would an investor’s portfolio look like if they had bought these bonds?

— Let us assume that on July 13, 2022, an investor purchased Ukrainian bonds at a price of 15,7% of face value, paying $1,570. Over 3.5 years, amid expectations of a peace agreement, the bond price increased to 62,1% of face value. As a result, over 3.5 years the investor’s price gain (i.e., total profit) amounted to $4,640, with a total return of approximately +295.5% over the period, or an annualized return of about 84%. It is important to understand that this example illustrates market mechanics only, and we do not recommend engaging in such strategies without a deep understanding of the associated risks and scenarios. Such trades fall into the category of aggressive trading in distressed assets. Prices here are driven less by fundamental cash flows and more by the news agenda, political statements, and shifts in expectations regarding negotiations and restructuring. As a result, such portfolios are extremely volatile, highly sensitive to any negative headline, and can easily lose tens of percent within just a few days.

On February 4, Euroclear announced that it would transfer €1.4 billion to Ukraine from income generated by the placement of frozen Russian assets. Did this also affect investor sentiment?

— Indeed, this development may add confidence to Ukraine’s sovereign securities. Frozen Russian assets are held at the Euroclear depository. These funds cannot be returned to their owners due to sanctions, but they can be temporarily invested to earn interest. Euroclear does not earn money on the assets themselves, but on the interest generated from their placement. For example, in 2025 the depository earned around €5 billion. Under EU rules governing the institution, the majority of this amount is considered excess profit and may be allocated to support Ukraine.

What conditions has Ukraine been required to meet in order to receive these funds?

— In July 2025, Ukraine received €1.6 billion, and a further €1.4 billion will be transferred in 2026. The key point is that these funds are non-debt financing and do not need to be repaid.

How can Ukraine use these funds, and how does this affect investors?

— These funds help Ukraine cover budget expenditures and reduce its need for borrowing. For investors and markets, this is a signal that the country has a regular external source of funding rather than one-off promises of aid. Europe is using interest income from frozen Russian assets to provide ongoing support to Ukraine’s budget. This is already a functioning financial mechanism. In addition, on January 22, 2026, international rating agency S&P upgraded Ukraine’s credit rating from SD (selective default) to CCC+. This followed the completion in December 2025 of the restructuring of GDP-linked warrants totaling $2.6 billion. Simply put, Ukraine has formally exited default status on its key debt obligations. Thanks to the revised debt terms, the burden on the budget has been significantly reduced: annual debt servicing requirements are now around $1 billion. At the same time, repayments of principal will not begin before 2029, giving the state several years of financial breathing space and reducing near-term risks to the economy.